Geopolitical Energy Containment: Operation Epic Fury and the Strategic Reconfiguration of the Persian Gulf – China Axis

The military operations initiated on February 28, 2026, collectively designated as Operation Epic Fury, represent more than a localized conflict between the United States, Israel, and the Islamic Republic of Iran. This kinetic engagement serves as the catalyst for a fundamental restructuring of the global energy architecture, specifically designed to dismantle the Sino-Iranian energy nexus and integrate Persian Gulf resources into a Western-aligned economic framework.1 The fall of the Iranian regime, long a stated objective of the Trump administration and Israeli security hawks, is the essential prerequisite for a broader geopolitical strategy of “energy containment” directed at the People’s Republic of China.1 By forcibly altering the volume, direction, and pricing of Iranian oil exports, the U.S.-led coalition seeks to terminate the multi-billion-dollar “sanctioned barrel” subsidy that has insulated Chinese manufacturing from global price shocks.2

The Kinetic Catalyst: Operation Epic Fury and the Collapse of the Islamic Republic

The launch of combat operations on February 28, 2026, followed a terminal breakdown in the Omani-mediated negotiations that had persisted throughout 2025.5 While early rounds of talks in Muscat and Rome suggested a potential freeze on uranium enrichment in exchange for partial sanctions relief, the emergence of a new Iranian ballistic missile program and continued Houthi strikes on Red Sea shipping created an intolerable security environment for Washington and Jerusalem.6 Operation Epic Fury was thus conceived not merely as a punitive strike but as a comprehensive campaign to topple the ideological state.1

The initial waves of the assault targeted the command-and-control nodes of the Islamic Revolutionary Guard Corps (IRGC) and the Supreme National Security Council.5 Israeli decapitation strikes reportedly neutralized the top echelon of the Iranian leadership, including confirmed reports regarding the death of Supreme Leader Ali Khamenei and Defense Minister Aziz Nasir Zadeh.1 The degradation of the Iranian military was unprecedented in its scope, aiming to “annihilate” the navy and “raze” the missile industry to prevent the asymmetric retaliation that has long defined Iranian deterrence.1

| Targeted National Entity | Strategic Function | Outcome of Operation Epic Fury |

| Supreme Leadership (Khamenei) | Ideological/Political Command | Reported Neutralized 1 |

| IRGC Ground/Naval Forces | Regional Proxy Support/Hormuz Control | Significant Degradation/Assets Sunk 5 |

| Asaluyeh & Kharg Island | Primary Oil Export Infrastructure | Shut Down/Infrastructure Damage 8 |

| South Pars Gas Field | 80% of Domestic Gas Production | Major Disruptions/Fires 8 |

| National Information Network | Domestic Surveillance/Censorship | Fragmented/Communication Blackout 9 |

The collapse of the regime’s centralized authority has triggered a transition from a functioning, if isolated, state to a condition of regime collapse, characterized by the inability to control the currency or provide basic utilities.10 In the resulting vacuum, the strategic focus has shifted from the battlefield to the global oil markets, where the termination of the Islamic Republic’s “Look East” policy has created an opening for the forced redirection of Iranian hydrocarbons toward the European Union.12

The Architecture of Chinese Dependency: The Sanctioned Barrel Mechanism

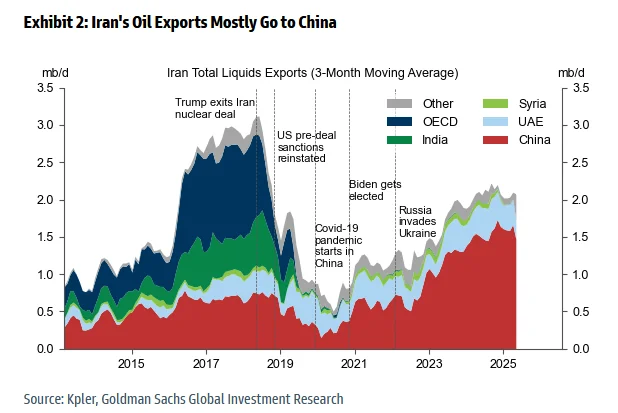

To understand the strategic logic of weakening China through Iranian regime change, one must first analyze the structural dependency Beijing developed on Tehran during the era of maximum pressure. Throughout 2024 and 2025, China emerged as the primary lifeline for Iran’s economy, absorbing over 80% of Iran’s total oil exports.3 By early 2026, Iranian deliveries to China reached approximately 1.38 million barrels per day (bpd), accounting for roughly 13.4% of China’s total seaborne crude imports.2

This relationship was not merely transactional; it was an exercise in “energy arbitrage.” Because Iranian oil was under U.S. sanctions, it was sold to Chinese independent refiners—known as “teapots”—at steep discounts ranging from $8 to $10 per barrel below global benchmarks such as Brent or Oman.2 This “sanctioned barrel” provided China with a marginal advantage in global manufacturing by lowering the energy input costs for its industrial base.2

The pricing mechanism can be expressed as:

Where PChina is the effective price paid by Chinese refiners, PBrent is the market benchmark, DSanction is the discount offered by Tehran (typically $8-$10), and CShadow is the cost of operating the shadow tanker fleet and intermediary banking networks.2 Despite the costs of evasion, the net savings for Beijing were estimated at over $10 billion annually.3

| China’s Oil Import Profile (2025) | Volume (Million bpd) | Reliance Mechanism | Strategic Vulnerability |

| Russia | 2.1 – 2.6 | Pipeline/Seaborne | High (Sanction Exposure) 17 |

| Saudi Arabia | 1.7 | Long-term Contracts | Moderate (U.S. Alliance) 17 |

| Iran | 1.38 | Shadow Fleet/Discounted | Extreme (Regime Stability) 2 |

| Malaysia (Relabeled) | 1.3 | Ship-to-Ship Transfers | High (Chokepoint Risk) 17 |

| Brazil | 0.8 | Market Purchases | Low (Neutral Partner) 17 |

The fall of the Iranian regime represents the termination of this subsidy. A post-revolutionary government seeking international legitimacy and the release of frozen assets would necessarily shift toward a transparent, market-priced export model.13 This shift effectively imposes a tax on the Chinese economy by removing the discount that has fueled its post-COVID industrial recovery.2

The Theory of European Substitution: Filling the Exporting Vacuum

A primary hypothesis in the post-war strategic planning is the “Addition of Europe” to the Iranian export equation. In this scenario, the volumes previously earmarked for China are redirected to the European Union, which has been seeking a definitive alternative to Russian hydrocarbons since the 2022 invasion of Ukraine.13 The reintegration of Iran into the global economy is projected to increase Iran’s real GDP by over 80% in the long term, while simultaneously boosting EU GDP by 0.3% to 0.5% through reduced energy volatility.13

The redirection theory posits that by integrating Iran into the Southern Gas Corridor (SGC) and upgrading its refinery infrastructure with Western technology, the U.S. can create a “virtuous cycle” of energy security.21 Iranian crude and natural gas would flow westward through Turkey and the Mediterranean, replacing the “missing” Russian volumes and allowing the U.S. to focus its own crude exports on Asian allies—such as Japan and South Korea—thereby outbidding China for the remaining global supply.20

This strategy serves two critical functions. First, it stabilizes the Eurozone economy, making it more resilient to Chinese industrial competition.13 Second, it deprives China of its primary non-Western energy partner.2 The logic of the “European Vacuum” suggests that the global market will naturally rebalance: as Europe absorbs Iranian oil, the U.S. and OPEC+ members like Saudi Arabia and the UAE can leverage their spare capacity to control the price and availability of oil in the Pacific theater.23

The ICIS Gas Foresight modeling indicates that a return of Iranian energy to the global market would not only lower prices but also reduce the “Hormuz Risk Premium” that currently inflates global energy costs.26 For Europe, Iranian gas represents a “high-volume, low-risk” alternative that utilizes existing and planned pipeline infrastructure, such as the expanded Trans-Adriatic Pipeline (TAP).20

Monetary Decoupling: The Collapse of the Petroyuan and the Rial

The relation between the war and the strategy to weaken China extends into the monetary realm. For years, the Iranian regime was a pioneer in using the “Petroyuan,” conducting oil trades in Renminbi to bypass the SWIFT system and the U.S. dollar.27 This was central to China’s broader strategy of internationalizing its currency and challenging the Petrodollar standard established in the 1970s.27

The fall of the Islamic Republic effectively terminates this experiment. A transitional government in Tehran would require access to the U.S. dollar-dominated global financial system to facilitate economic reconstruction and attract foreign direct investment (FDI).13 The collapse of the Rial, which saw its value evaporate as the state lost control over currency allocation, provides a stark lesson in the risks of decoupling from the Western financial order.10

| Currency System | Mechanism of Dominance | Impact of Iranian Regime Change |

| Petrodollar | U.S. Saudi Accord/SWIFT | Restored as Exclusive Medium for Gulf Oil 27 |

| Petroyuan | Bilateral Barter/Renminbi Futures | Terminated/Loss of Strategic Partner 27 |

| Shadow Banking | Shell Companies/Dark Fleet | Dismantled by Kinetic/Financial Pressure 10 |

| Iranian Rial | Centralized Subsidy/Dual Rates | Total Collapse/Replacement by Transitional Currency 10 |

The destruction of the shadow banking system, which Iran used to manage its foreign exchange reserves through extraterritorial networks, represents a major intelligence and financial blow to Beijing.10 Without the Iranian nexus, China’s ability to conduct large-scale, sanction-immune trade with other “pariah” states is significantly diminished, reinforcing the hegemony of the U.S. financial system as the sole arbiter of global trade.2

Connectivity Wars: IMEC vs. the Belt and Road Initiative

The post-regime change strategy also involves a fundamental shift in regional infrastructure. Under the 25-Year Agreement, Iran was a cornerstone of China’s Belt and Road Initiative (BRI), offering a land-based alternative to the “Malacca Dilemma”—the fear that the U.S. Navy could blockade the Malacca Strait during a conflict.14 The development of Iranian ports and railways was intended to create a “Eurasian Land Bridge” that would secure Chinese access to the Persian Gulf and the Mediterranean.9

The fall of the regime and the subsequent military degradation of Iranian coastal assets at Asaluyeh and Bandar Abbas have effectively checkmated this strategy.8 In its place, the United States is promoting the India-Middle East-Europe Economic Corridor (IMEC), which positions Israel and India as the primary anchors of a new, transparent, and Western-aligned trade route.31

IMEC serves as a “geopolitical alternative” to the BRI by embedding trade and energy routes within a framework of security and political alignment.31 With a new, pro-Western government in Tehran, Iran could be integrated into IMEC, providing the corridor with direct access to massive natural gas reserves and a terrestrial link between the Indian Ocean and the Caspian Sea.31 This would marginalize the Russian-backed International North-South Transport Corridor (INSTC) and leave China’s BRI projects in the region as “stranded assets”.9

The U.S. Swing Producer Strategy and Strategic Reserves

A critical component of the strategy to isolate China is the role of the United States as a global energy stabilizer. In the event of the short-term market volatility expected during the regime’s collapse, the U.S. Strategic Petroleum Reserve (SPR) acts as a primary tool of economic warfare.25 With a drawdown capacity of 4.4 million bpd, the SPR can provide temporary market support to allies in Europe and Asia, preventing the “mother of all bidding wars” from spiraling out of control.25

By 2026, the U.S. is forecast to be a dominant exporter of crude and LNG, with the capacity to fill the supply gaps left by the disruption of Iranian exports to China.24 The strategic logic is to use U.S. volumes to “reward” compliant nations while allowing “adversarial” nations—like China—to bear the brunt of the market’s physical tightness.2

| Energy Security Asset | Capacity / Volume | Strategic Deployment |

| U.S. SPR | 415 – 714 Million Barrels | Market Stabilization/Price Dampening 25 |

| Chinese Crude Stocks | 1.2 Billion Barrels | Short-term Buffer (104 Days) 17 |

| OPEC+ Spare Capacity | 4.0 – 5.0 Million bpd | Targeted Production Increases 8 |

| UAE/Saudi Pipelines | 1.8 – 5.0 Million bpd | Hormuz Bypass for Ally Exports 35 |

While China has built significant strategic stockpiles—estimated at over 1.2 billion barrels—this only provides a multi-month cushion against disruption.17 Once these reserves are depleted, Beijing will be forced to compete in a global market where the U.S. and its partners control the primary surplus capacity.2 This “energy enclosure” strategy effectively subordinates Chinese industrial growth to Western energy policy.2

Chinese Resilience and the 15th Five-Year Plan

China’s response to this mounting energy containment is codified in its 15th Five-Year Plan (2026-2030). Beijing has recognized the increasing volatility of the global environment and is pivoting toward “New Quality Productive Forces,” emphasizing technological self-reliance, industrial upgrading, and domestic supply chain resilience.19 The Plan underscores a shift away from reliance on an “uncertain global environment” and toward the internal consolidation of power.19

To mitigate the loss of Iranian oil, China is doubling down on:

- Renewable Dominance: Expanding its lead in solar, wind, and battery energy storage systems to reduce the “floor” of its crude oil demand.39

- Strategic Diversification: Increasing imports from “low-risk” suppliers like Brazil and Russia, while expanding domestic production in regions like Xinjiang and Inner Mongolia.17

- Nuclear Baseload: Rapidly expanding nuclear capacity—now the world’s largest—to provide a stable alternative to gas-fired power.39

However, these efforts face significant structural headwinds. The phenomenon of “involution”—excessive domestic competition that drives down profits—and the ongoing property slump have weakened the Chinese middle class and reduced the state’s fiscal space to subsidize a rapid energy transition.39 The “energy shock” triggered by Operation Epic Fury thus hits China at a moment of acute internal vulnerability.19

Second-Order Effects: Regional Stability and the “credibility floor”

The fall of the Iranian regime also forces a realignment among other regional powers. Russia and China, which have positioned themselves as “alternative security guarantors” to the West, face a “credibility floor”.14 If they fail to move beyond a transactional role and actively safeguard their remaining partners—such as the battered Syrian government or the central Asian states—they risk being perceived as “unreliable guarantors”.14

The collapse of the Sino-Iranian axis leaves Russia as China’s only major partner in Eurasia.14 This increases Beijing’s dependency on Moscow for energy and overland transit, potentially creating a “subordinate alliance” that the United States can exploit through secondary sanctions.2 Conversely, the addition of a post-revolutionary Iran to the “Western column” creates a contiguous block of U.S.-aligned states from the Mediterranean to the Indus River, completing the “Great Encirclement” of the Eurasian heartland.2

Synthesis and Strategic Outlook

The war between the U.S.-Israeli coalition and the Islamic Republic of Iran is the definitive geopolitical rupture of the 2020s. While the kinetic operations of February 28, 2026, were directed at the immediate threats of nuclear proliferation and regional proxy warfare, the ultimate objective is the recalibration of the global energy balance.1

By toppling the regime, the U.S. achieves four critical strategic goals:

- Industrial Attrition: It imposes higher energy costs on China by terminating the discounted “sanctioned barrel” and forcing Beijing into the transparent global market.2

- European Stabilization: It provides the European Union with a permanent, non-Russian energy alternative, strengthening the transatlantic alliance and facilitating the “addition of Europe” as a primary Iranian customer.13

- Monetary Hegemony: It collapses the Petroyuan experiment and restores the dollar as the exclusive medium of exchange in the Persian Gulf.27

- Infrastructure Dominance: It checkmates the Belt and Road Initiative by replacing the Iranian bridgehead with the IMEC corridor, ensuring that future Eurasian trade is conducted on Western terms.14

The transition to a post-regime-change world will be marked by short-term price volatility and the constant threat of asymmetric retaliation from “IRGC-istan”—the fragmented remnants of the security apparatus.7 However, the structural shifts in oil exporting volumes, currency usage, and infrastructure alignment suggest that the 2026 conflict has effectively modulated China’s economic trajectory for the next decade, reinforcing the continued relevance of the U.S.-led global order.2 The Middle East remains the “geopolitical fulcrum” where localized conflicts serve as the primary instruments of global statecraft.2

Works cited

- Gauging the Impact of Massive U.S.-Israeli Strikes on Iran | Council …, accessed March 1, 2026, https://www.cfr.org/articles/gauging-the-impact-of-massive-u-s-israeli-strikes-on-iran

- (PDF) The Tehran-Beijing Nexus: Iran as the Geopolitical Fulcrum of …, accessed March 1, 2026, https://www.researchgate.net/publication/401315091_The_Tehran-Beijing_Nexus_Iran_as_the_Geopolitical_Fulcrum_of_US_Energy_Containment_Strategies_against_China

- China’s Dependence on Iranian Oil: Strategic Leverage and …, accessed March 1, 2026, https://moderndiplomacy.eu/2026/01/13/chinas-dependence-on-iranian-oil-strategic-leverage-and-exposure/

- Iran’s Discounted Oil, Beijing’s Risky Addiction | FinancialTribune, accessed March 1, 2026, https://financialtribune.com/node/119583

- Iran Update Special Report: US and Israeli Strikes, February 28, 2026, accessed March 1, 2026, https://understandingwar.org/research/middle-east/iran-update-special-report-us-and-israeli-strikes-february-28-2026/

- 2025–2026 Iran–United States negotiations – Wikipedia, accessed March 1, 2026, https://en.wikipedia.org/wiki/2025%E2%80%932026_Iran%E2%80%93United_States_negotiations

- Experts react: The US and Israel just unleashed a major attack on Iran. What’s next?, accessed March 1, 2026, https://www.atlanticcouncil.org/dispatches/experts-react-the-us-and-israel-just-unleashed-a-major-attack-on-iran-whats-next/

- Iranian Oil and Gas Infrastructure – Geopolitical Futures, accessed March 1, 2026, https://geopoliticalfutures.com/iranian-oil-and-gas-infrastructure/

- Iran–China 25-year Cooperation Program – Wikipedia, accessed March 1, 2026, https://en.wikipedia.org/wiki/Iran%E2%80%93China_25-year_Cooperation_Program

- The Ayatollah’s Regime Is Crumbling | Hudson Institute, accessed March 1, 2026, https://www.hudson.org/foreign-policy/ayatollahs-regime-crumbling-michael-doran

- The state of the Iranian regime after protests – Johns Hopkins University, accessed March 1, 2026, https://washingtondc.jhu.edu/news/what-to-know-about-iran-february-2026/

- China is playing the long game over Iran | Chatham House – International Affairs Think Tank, accessed March 1, 2026, https://www.chathamhouse.org/2026/02/china-playing-long-game-over-iran

- Regime Change in Iran Could Boost EU Economy – WIFO, accessed March 1, 2026, https://www.wifo.ac.at/en/news/regime-change-in-iran-could-boost-eu-economy/

- How Russian and China Tech Underpins Iranian Strategic Depth, accessed March 1, 2026, https://www.specialeurasia.com/2026/03/01/russia-china-iran-tech-military/

- Iran’s energy trade defies year of US maximum pressure sanctions, accessed March 1, 2026, https://www.iranintl.com/en/202601226536

- Growing but Limited: Iranian Economic Relations with China | INSS, accessed March 1, 2026, https://www.inss.org.il/publication/china-iran-economy/

- Where China Gets Its Oil: Crude Imports in 2025 Reveal Stockpiling and Changing Fortunes of Certain Suppliers, Including Those Sanctioned – Center on Global Energy Policy at Columbia University SIPA | CGEP %, accessed March 1, 2026, https://www.energypolicy.columbia.edu/where-china-gets-its-oil-crude-imports-in-2025-reveal-stockpiling-and-changing-fortunes-of-certain-suppliers-including-those-sanctioned/

- The alternative to regime change: Changing the regime’s behavior – Middle East Institute, accessed March 1, 2026, https://mei.edu/publication/alternative-regime-change-changing-regimes-behavior/

- China’s Fifteenth Five-Year Plan: Stability, Modernization, and the Strategic Logic Behind Its Domestic Priorities – ICAS, accessed March 1, 2026, https://chinaus-icas.org/research/chinas-fifteenth-five-year-plan-stability-modernization-and-the-strategic-logic-behind-its-domestic-priorities/

- The geopolitics of energy in Europe: Short-term and long-term issues – Funcas, accessed March 1, 2026, https://www.funcas.es/articulos/the-geopolitics-of-energy-in-europe-short-term-and-long-term-issues/

- (PDF) The EU’s Botched Geopolitical Approach to External Energy Policy: The Case of the Southern Gas Corridor – ResearchGate, accessed March 1, 2026, https://www.researchgate.net/publication/322091707_The_EU’s_Botched_Geopolitical_Approach_to_External_Energy_Policy_The_Case_of_the_Southern_Gas_Corridor

- Iranian gas export potential to Europe after JCPOA and existing directions of Turkmenistan energy resources transportation and supply diversification., accessed March 1, 2026, https://www.unectf.org/en/iranian-gas-export-potential-to-europe-after-jcpoa-and-existing-directions-of-turkmenistan-energy-resources-transportation-and-supply-diversification-2/

- Iran Nuclear Negotiations Reshape Global Oil Market Dynamics – Discovery Alert, accessed March 1, 2026, https://discoveryalert.com.au/iran-nuclear-negotiations-oil-market-volatility-2026/

- Short-term energy outlook (EIA), accessed March 1, 2026, https://www.eia.gov/outlooks/steo/report/global_oil.php

- China and U.S. Oil Stockpiles Could Cushion an Iran Supply Shock | Investing.com, accessed March 1, 2026, https://www.investing.com/analysis/china-and-us-oil-stockpiles-could-cushion-an-iran-supply-shock-200675703

- Potential Strait of Hormuz closure could push Europe’s TTF gas benchmark above €90.00/MWh – ICIS analysts | ICIS, accessed March 1, 2026, https://www.icis.com/explore/resources/news/2026/02/28/11184028/potential-strait-of-hormuz-closure-could-push-europe-s-ttf-gas-benchmark-above-90-00-mwh-icis-analysts/

- What is the petroyuan? – CurrencyTransfer, accessed March 1, 2026, https://www.currencytransfer.com/blog/expert-analysis/what-is-the-petroyuan

- Geopolitics of Oil: How China is Challenging the Petrodollar through the Pedro-Yuan, accessed March 1, 2026, https://ipr.blogs.ie.edu/2025/06/27/geopolitics-of-oil-how-china-is-challenging-the-petrodollar-through-the-pedro-yuan/

- The “One Belt, One Road” Strategy and China’s Energy Policy in the Middle East, accessed March 1, 2026, https://mei.edu/publication/one-belt-one-road-strategy-and-chinas-energy-policy-middle-east/

- China’s Middle East Strategy in 2025: Between Iran and Israel – Beyond the Horizon ISSG, accessed March 1, 2026, https://behorizon.org/between-tehran-and-tel-aviv-chinas-strategic-balancing-act-in-the-middle-east/

- India is central to Israel’s new strategic architecture | The Jerusalem Post, accessed March 1, 2026, https://www.jpost.com/opinion/article-887722

- India and Israel: Strategic Convergence in a Changing World, accessed March 1, 2026, https://jstribune.com/india-and-israel-strategic-convergence-in-a-changing-world/

- The Belt and Road Initiative Ten Years On: China and the Middle East in a Changing Geopolitical Landscape, accessed March 1, 2026, https://mecouncil.org/wp-content/uploads/2024/10/The-Belt-and-Road-Initiative-Ten-Years-On-Report.pdf

- Strait of Hormuz Closure: Global Energy Market Impact – Discovery Alert, accessed March 1, 2026, https://discoveryalert.com.au/chokepoint-economics-geography-weaponry-2026-strategic-vulnerability/

- How the attack on Iran could impact the global oil market and …, accessed March 1, 2026, https://www.cnbcafrica.com/2026/how-the-attack-on-iran-could-impact-the-global-oil-market-and-economy

- Oil Price Forecast for 2026 | J.P. Morgan Global Research, accessed March 1, 2026, https://www.jpmorgan.com/insights/global-research/commodities/oil-prices

- How the Iran Conflict Will Impact Global Oil Shipments by Country – Energy News Beat, accessed March 1, 2026, https://energynewsbeat.co/how-the-iran-conflict-will-impact-global-oil-shipments-by-country/

- Fourth Plenum 2025: Xi Jinping’s Strategic Roadmap to 2030 – Beyond the Horizon ISSG, accessed March 1, 2026, https://behorizon.org/fourth-plenum-2025-setting-chinas-course-to-2030/

- China Economic Consolidation and Strategic Shifts in 2026 – CKGSB Knowledge, accessed March 1, 2026, https://english.ckgsb.edu.cn/knowledge/article/china-economic-consolidation-and-strategic-shifts-in-2026/

- China’s Economic Strategy in 2026 to Prioritize Continuity Over Change, accessed March 1, 2026, https://www.asiapacific.ca/publication/chinas-economic-strategy-2026-prioritize-continuity-over-change

- China refiners turn to Russian oil as Iran faces rising uncertainty, accessed March 1, 2026, https://www.iranintl.com/en/202602252742

Reflections on the American-Israeli War on the Mullahs of Iran | Mohamed Chtatou | The Times of Israel – The Blogs, accessed March 1, 2026, https://blogs.timesofisrael.com/reflections-on-the-american-israeli-war-on-the-mullahs-of-iran/